Phantom Income, A Millionaire’s Secret Formula

In a country of growing inequality it’s easy to gang up on the wealthy, the 1%ers, the landlords. Unfortunately, most conversations on the topic take an immediate turn in the wrong direction and before we know it we’re discussing Republicans and Democrats. The answer is much simpler than the talking points on cable news. The very simple reason why some peoples’ extraordinary wealth grows significantly against the average American, thus creating a wealth gap, is because of math. Let’s consider two concepts.

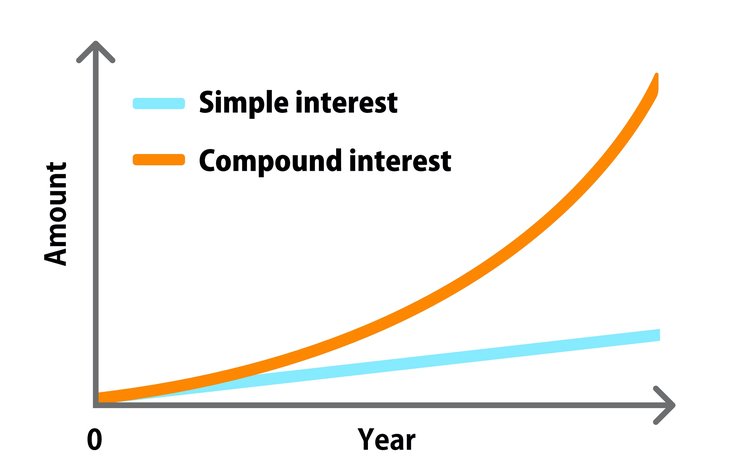

Most people understand compound interest in the form of credit card or student loan debt, seeing it snowball into much larger amounts than when it was first created. Another concept understood by most people is how “Back in my day a soda only cost a nickel!'“ Otherwise known as inflation. These two principles are responsible for a jaw dropping amount of money leaving the pockets of the average American. Whether it’s the stacking up of debt or the draining of purchasing power, compound interest and inflation deplete funds on a global level. But what if instead of acting against your wallet, it was there to help you. How could this be possible? Please welcome my two guests - appreciation and compound interest.

Liabilities create inflation for the owner while assets create appreciation. The cost of hamburgers costs more each year because it is a liability for you, albeit a necessary one. Your rental property on the other hand appreciates each year to a higher value, because of the same exact principle. Compound interest is a life changing tool that takes dedication, discipline, and a most elusive trait in 2022 - patience. If you are able to put money into assets year after year the value of those assets, due to inflation, (cough cough) sorry, appreciation takes the value into hyperdrive and creates exponential growth.

Compound interest equals exponential growth. Notice the GAP it creates from those not utilizing it.

Math + Materials

Ok, so math is one thing but there are obviously a lot more practical applications of government regulations, tax incentives, and human interactions involved in Real Estate. Maybe the best and most notorious example of how the rubber meets the road when it comes to real estate and practical application of it is when Donald Trump was pressed on the issue of how a man worth several billion dollars could only pay a few hundred dollars in federal income tax. His reply: ‘That makes me smart.’ And whether you hate the man’s guts or not, he’s right. How is it then that a person, or company, can pay little to no income tax when receiving hundreds, thousands, and (I hate to break it to you) even millions of dollars from real estate income? It all starts with knowing the rules and learning to play the game within them. The game is life, and the rules are in the IRS tax-code. Don’t hate the player, hate the game.

In the United States of America there is no other entity that has more favorable tax treatment that real estate. Although this is the topic of an entirely different conversation, the main reason for taxation is NOT to pay for the Government’s bills. Do you think our taxes paid for any of the stimulus bills? Covid relief? No, the Fed just printed money out of thin air and paid the bill. In fact in 2021 the government made $4 trillion dollars but spent $6.8 trillion. IN FACT since 1972 the average deficit (revenue-expenses) has been 3.5%. (See US Budget Infographic here) Ok, don’t get me started…

The point is, taxes don’t cover the whole bill and are primarily meant to encourage and discourage human behavior. There are taxes on sugar, plastic bags, alcohol, and much more, all intended to curb consumption. On the flip side there are tremendous tax incentives available to ALL CITIZENS just waiting to be taken advantage of. Let’s consider a few real estate incentives and how they can make you seriously wealthy over time.

(Compound Interest + Tax Incentives) x Real Estate = The answer

Compound Interest can best be explained like this… If you put $60,000 away in an account earning 12% interest per year, in 20 years you’d have $578,000 having never added another penny to the account after day 1. Yea…

Tax Incentives help mainly on the expenses end. So if you had a $578,000 paper income from real estate you can use many of the methods in this article to make that number at or below 0$. (What Trump did to pay no taxes)

Real Estate utilizes both of these principles and also allows for monthly income in the form of rent. It’s like having your cake and eating it too.

The government wants people to build houses because we as a society recognize that people need places to live. What the government does not want to do is build or manage housing themselves, mainly because they suck at it. Incentivizing private citizens to build homes for the government, the IRS allows for some serious savings and wealth building opportunities. When considering these various incentives it is important to understand the difference between a paper value and a real value. Paper value (where most of the incentives are) are only seen on paper and are not realized until a property is sold. For example if your home appreciates from one year to the next, you don’t actually get the additional money until you sell your home. This is also seen on your tax return where depreciation, for example, can take the actual money you make and on paper, lower or remove it so you don’t owe any taxes. Not every dollar is created equal. Let’s dive in.

Depreciation

A real estate investor is allowed to depreciate the building value (not the land) over 27.5 years for residential properties and 39 years for commercial properties. Sorry, no you cannot depreciate your personal residence, it must be an investment property. It works like this… Say the fair market value of your BUILDING value is $200,000. $200,000 / 27.5 = $7,272. $7,272/12 = $606 / month. This means if you have a rental property and are cash flowing $500 / month, after depreciation, according to the IRS you are actually losing ($606-$500) $106 dollars a month. Without depreciation you would have been paying 22% tax rate (the average) on $6,000 / year in income leaving you with a $1,320 tax burden. WITH depreciation you are actually ‘losing’ $1,272 / year and can deduct that amount from your taxable income. Basically giving yourself a $280 tax credit. That’s a $1,600 swing!

The beauty of depreciation is the cash flow income you are actually receiving ($500 / month) stays in your pocket and you can buy all the soy lattes your heart desires. The $280 tax credit you receive is only on PAPER and will not truly affect you until it comes time to pay taxes. This is the first step to understand how you can pay little to no federal income tax. Imagine this on a larger, dare I say compounded, scale with a few more 0’s at the end of each number. The principle remains the same whether it is 1 house or 100. If you had 10 properties with this exact same setup that would mean you are generating $5,000 / month in real dollars, in your pocket, but at the end of the year the government is saying THEY owe YOU $2,800.

The Cash Out Refinance

Most people are aware of the ability to refinance your home and receive a new interest rate. If the current market interest rates are lower than your current rate, you can go to the bank and ask to refinance. You will pay closing costs and get a brand new loan with new terms but this time paying less money each month. A cash out refinance is different because you are refinancing the property, but with the added benefit of the bank writing YOU a check. Say you own a rental property that has seen enormous appreciation over the past few years or you have remodeled it and the value is higher. Let’s pretend initially you had an $80,000 loan on a $100,000 property but now that your house is worth $200,000 you want to get a cash out refinance. The bank will finance approximately 80% LTV (Loan to Value) or $160,000 meaning they will literally write you a check with your name on it for $160,000 - previous loan amount, which in this case equals $80,000. You take the check and deposit it into your checking account. It is yours and technically you can do whatever you want with it. As a smart investor you are going to use it to buy more income producing properties.

The BRRRR method, coined by one of Bigger Pockets founders is the epitome of a genius real estate strategy. BRRRR = Buy, Rehab, Refinance, Rent, and Repeat. In a nutshell you buy a property below market value, add value to it by rehabbing it, refinance at the new ARV (after repair value), and rent it out. Then repeat. Sounds simple enough but let’s peel beneath the surface to really see how and why this strategy can make you a millionaire.

Let’s say you find a great off-market deal for $50,000 and put $30,000 into rehabbing the house. After turning a dump into a beautiful new property the bank says it is appraised for $130,000. This means the bank will write you a check for $104,000 (80% LTV). You have now made $104,000 - $50,000 purchase - $30,000 rehab - $2,500 (closing & holding costs) =$21,500. When all is said and done you will have in your hand $21,500 in cash and the keys to a brand new fixed up home. AND $26,000 in equity ($130,000 - $104,000). OK, now comes the ‘rent’ part. Even at 8% your Principle and interest for the $104,000 loan is about $610. Since this is in a desirable neighborhood you are able to get $1,200 / month in rent meaning you will cash flow about $1,200-$610-$250 (Insurance, tax, ect.) = $340. (Remember what we can do about this via depreciation.)

Off of this ONE deal we are seeing:

$26,000 in equity

$21,500 cash in hand

$340 in real monthly cash flow

$303 in depreciation / month (Making the taxable income $37 / month)

An appreciating asset currently valued at $130,000. With average yearly appreciation of 4% this home will be worth $158,000 in 5 years.

When all is said and done it did not end up costing one single penny. Although there are several ‘best parts’ we need to take a look at the hero of this whole equation. ALERT: This is the part where you Dave Ramsey people may need to go outside and play for a while. Because the hero is debt.

Debt

Debt is a very misunderstood and even more-so abused tool in America. For the sake of attention spans we will not go into the whole theory of debt but just stick with the practical application as it pertains to real estate. Debt is leverage and debt is a tool. And debt is how you become a millionaire. In the BRRRR strategy when you refinance and receive that check from the bank, the money you are holding in your hand is debt. And because it is debt, it is NOT considered taxable income. I repeat, you are not taxed on debt. If that sentiment does not make your eyes open wide with opportunity then let me phrase it a different way. When you refinance your property and the bank GIVES YOU MONEY, you do not have to pay taxes on it. Not stocks, not crypto, not art, nor baseball card investments allows for this magic. To truly see how powerful this is let’s compare two examples.

Let’s pretend you are single and make $100,000 a year before taxes. You are in the 24% tax bracket, your marginal tax rate is closer to 31%, but the average is about 22%. Confusing huh? The point is if you have a $100,000 salary you are paying about $22,000 in taxes. At this rate it would actually take you 3.32 months to NET $21,500 in your pocket, and during this span your gross income would be about $28,000. Put another way, if you want to make $21,500 you would need to gross $28,000 and actually do the work over 3.32 months. Phew, sounds terrible. On the other hand…

As our initial example pointed out you could cash out refinance $21,500 from our $130,000 property, but this time you are NOT taxed. You did not need to work for $28,000 in order to take home $21,500. In fact, after receiving this money not only do we still have a cash producing asset but it is lowering our tax bill via depreciation! This is all assuming an actual professional did the rehab, not you. In fact, you could have been surfing while all of this was taking place. Most people brush this off as if the math isn’t real. Sure there are some more intricacies left out for the sake of making the point, but this is real life, available to anyone, wealth creation. If we took the above two examples and fast forwarded over 10 years, assuming we acquire only 1 property per year, this is what we’d see.

W2 Worker - In 10 years would have earned $1,000,000 but only take home $776,000. And don’t forget about inflation which will take the buying power of this money down significantly. Without any assets this money is only worth less each year. Most importantly however, you have to do all the work. The second you stop working, you stop making money.

Investor - In 10 years, assuming 3% inflation, your total portfolio of 10 homes will consist of $1,500,000 in property value, $500,000 in Equity, and $225,000 in cash flow. This is NOT considering any depreciation and not putting that half million dollars of Equity to use in purchasing more properties. Not to mention it is assuming a low 3% inflation, never increasing the rent, and never finding better producing properties. You could stop working forever and keep making the same money.

In one scenario you are working for money and in the other the money is working for you.

Appreciation

As was mentioned in and throughout the previous examples we can’t discuss the benefits of real estate without appreciation. In times when inflation runs rampant those with liabilities yell INFLATION! But, during these same times, those with assets scream APPRECIATION! Inflation and appreciation are the same principle however inflation applies to liabilities and appreciation applies to assets. Our personal Real Estate strategy is not based on appreciation but it is certainly a part of the equation. In order to successfully utilize a cash out refinance we need the value of the property to increase. After our initial rehab this is almost only possible via appreciation.

Consider these facts: A $250,000 home is worth $606,000 after 30 years at 3% inflation. That same house however, is worth $810,000 during the same 30 years but at 4% inflation. What’s the average inflation rate for housing? From 1967-2022 it has been about 4.22%. Assuming this rate, thats an average of earning $20,000 per year on inflation alone. (Paper value) And that’s just one property so far.

The 1031 Exchange

There are many long lasting repercussions to most of the strategies listed above. Depreciation and refinancing can create a scenario where the tax bill is built up over the years until it comes due when selling out. This can be a significant bill. However, it can also be avoided and stopped in its tracks with the 1031 exchange. When you sell your personal residence you can often avoid paying capital gains tax however, selling an investment property will always incur a sales tax bill. The way to avoid it is to utilize the 1031 (IRS tax code) exchange which says you can take the funds from your sale and apply it to the purchase of a ‘like-kind’ new property and defer your tax bill.

Just as the cash out refinance was able to pull money out of debt and put it in your hands tax free, this method is a way to make phantom income. If we are to sell our $130,000 property we will owe a capital gains tax on the proceeds, in this case approximately $5,000. For a singular property at this price point the savings are not yet life changing but if we consider our 10 year plan to buy a home each year we would have saved over $100,000 during this time. Put back into our system, that equates to millions of dollars in investments.

Essentially this is what happens: You sell Property A and find Property B which you plan on buying with the proceeds. Since it is also real estate it is a ‘like-kind’ investment which is a requirement. You can trade from a house to a strip-mall or vice versa as long as it is real estate. You cannot transfer from real estate to a boat or a car or something like that. Within 45 days of the sale you must designate the new property for purchase and must close on the new property within 180 days of the initial sale. This can be done over and over again with no limitation. Although this strategy is not a way to put money in your hand as the cash out refinance does, it is real money that is being put towards a new property, leading to more money being put in your hand. Compounded again and again. Besides, saving $5,000 is the same thing as making an additional $5,000.

If you did this over the course of a lifetime you could save millions of dollars in tax payments. The down side is it does create a giant debt snowball which must be paid. With one exception… All the built up tax deferred payments you accrue over a lifetime go away when you die. Decent news for you but the best news for your kids. If selling out was an end goal then it is something to be considered however, a final sale before your death is not a requirement and you can certainly let it ride!

Circling Back to Compound Interest

You may have heard the old adage about how much a penny would be worth if you doubled it every day for 30 days. Answer: $5,368,000. This is a principle of compound interest, and although we are never expecting 100% annual returns (doubling) the concept is the same. The takeaway from this example however is that in the 30 day span, 75% of the wealth created comes in the final 2 nights. For many days it seems like nothing is happening and gains are minimal until finally… liftoff. This is how compound interest works and is why when our country saw the greatest levels of inflation in 40 years in 2022, the people with all the assets saw their wealth (not income) grow to exorbitant levels.

When you have assets and continue putting your gains back into the machine, eventually it will be printing money at levels you would not have dreamed when starting out. The best time to get started is 20 years ago. The next best time is right now.

Putting it all together

Yes, there are repercussions for using these strategies. The question is to determine how quickly you want to scale and how much risk you are willing to take on. Using accelerated depreciation early on will give you some serious benefits with cash flow, putting more cash in your pocket, allowing you to buy more properties in order to depreciate more, and thus putting more cash in your pocket.

None of this is intended to make you think that there is no work involved with Real Estate investing. Finding deals, coordinating with contractors, agents, property management, tenants, county tax assessors, lawyers, title offices, can be a lot of work and it is certainly time consuming. The point is, while you are doing these things there are several additional forces of nature at your back compounding your efforts. Working for a W-2 job even if it is at a high level is only one income stream. Real estate offers several streams, many of which are acting on your behalf while you sleep, day in and day out, year after year.